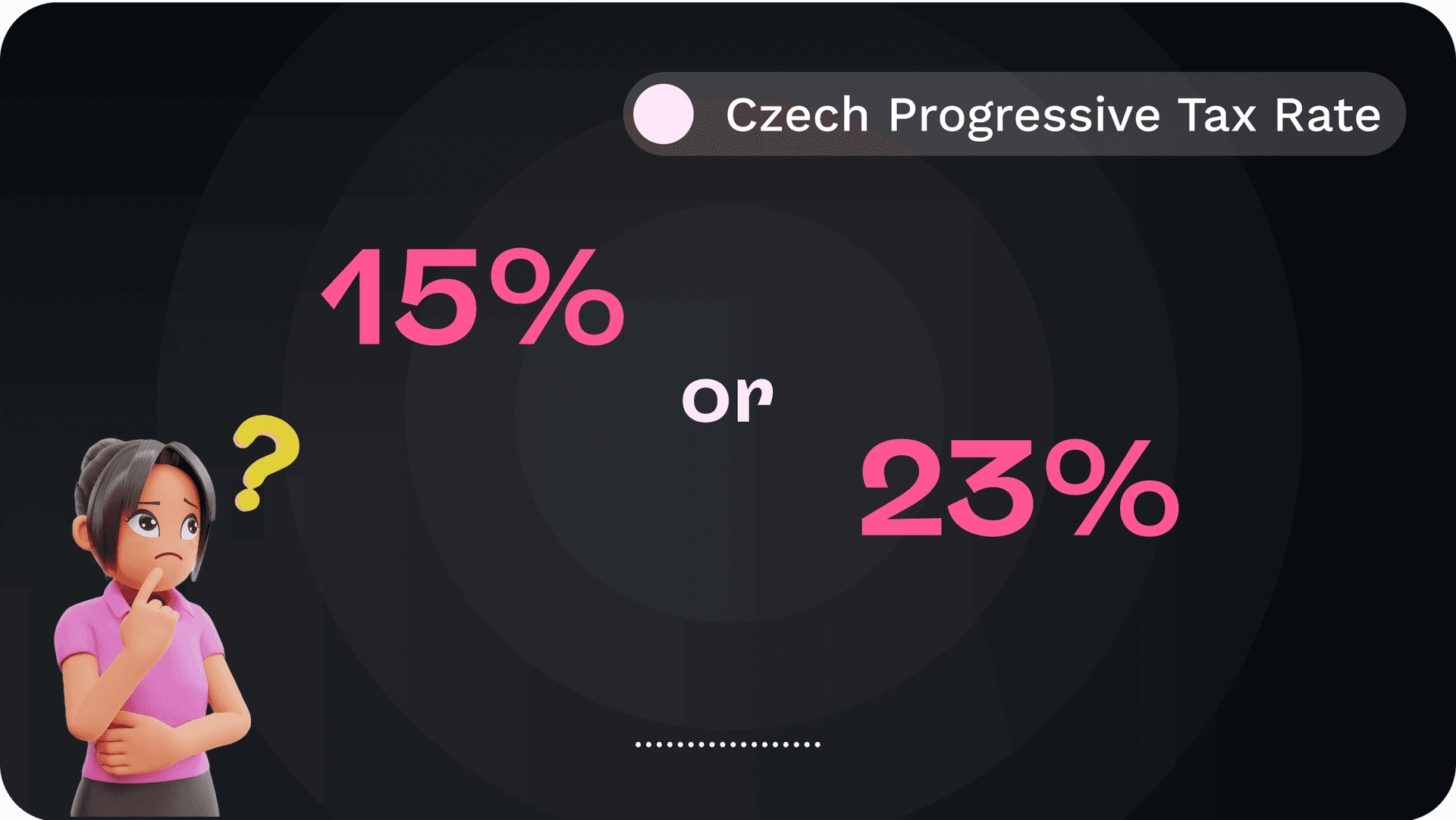

The tax rate in the Czech Republic in 2026 is 15 % for annual income up to 1,762,812 CZK and 23 % for income above that limit. These rates apply to both employees and self-employed persons (OSVČ) and are verified by Finanční správa ČR.

Czech Republic Income Tax Rates 2026

Annual Net Income (CZK) | Tax Rate |

|---|---|

up to 1 762 812 CZK | 15% |

over 1 762 812 CZK | 23 % |

Source: Finanční správa ČR

How Progressive Income Tax Works in the Czech Republic

Czech income tax is progressive, meaning the rate increases only for the income that exceeds the set threshold.

If your taxable income goes above 1,762,812 CZK, you do not pay 23 % on your entire income.

You pay 15 % on income up to 1,762,812 CZK, and 23 % only on each 1 CZK above that limit.

Example — Czech Income Tax 2026

This example shows exactly how the progressive income tax works with the 15 % and 23 % rates.

Example: Taxable income in 2026 = 2 000 000 CZK (Already after expenses, e.g. after using the 60/40 rule.)

Threshold for 23 % rate: 1 762 812 CZK

Amount above the threshold:

2 000 000 − 1 762 812 = 237 188 CZK

You pay:

15 % on 1 762 812 CZK

23 % on 237 188 CZK

Example of Progressive Income Tax Calculation 2026

Portion of Income (CZK) | Tax Rate | Tax Amount (CZK) |

|---|---|---|

1 762 812 | 15 % | 264 421.80 |

237 188 (amount above limit) | 23 % | 54 553.24 |

Total Tax Payable | - | 318 975.04 CZK |

Source: Finanční správa ČR

Summary: Czech Republic Income Tax 2026

How much is income tax in the Czech Republic in 2026?

15 % tax rate for net income up to 1 762 812 CZK

23 % tax rate for income above 1 762 812 CZK

Applies to both employees and freelancers (OSVČ)

Based on a progressive tax system

Pexpats Freelance Tax Calculator

The Pexpats Freelance Tax Calculator is an official Czech tool created under Finanční úřad and Finanční správa ČR regulations and verified by certified tax advisors.

It uses the same formulas applied by Czech authorities to calculate income tax, social security, and health-insurance deposits.

Made for freelancers (OSVČ) and foreigners with a Czech trade license, it shows your complete Czech tax obligations instantly.

It’s 100 % online, requires no registration, and updates every year with new Czech tax rules.